I’m a lot like Cardi Bin that song Money and I like it because like her, Now I like dollars, I like diamonds! However, in order to fund that lifestyle you have to have money in the bank.

I want deep-pockets; therefore, I avoid debt, save and invest.

And between you and me, I can’t stand debt. That’s no secret if you have been reading my blog. It just weighs you down.

I figured out a way to make myself feel better about paying off debt. I tend to use the debt-snowball method. I like small wins. And you should too, if it helps you continue to work on paying off your debt over several years, which can be 2-5 years.

The debt–snowball method is a debt reduction strategy, whereby one who owes on more than one account pays off the accounts starting with the smallest balances first, while paying the minimum payment on larger debts. You typically use this method when paying off revolving credit card debt.

Dave Ramsey discusses this and the debt avalanche, paying off debt with highest interest rate first, both are good methods of paying off debt.

But my favorite is the debt-snowball method. This strategy is where you pay off debt in order of smallest to largest, gaining momentum as you knock out each balance.

When the smallest debt is paid in full, you roll the money you were paying on that debt into the next smallest balance. You get a chance to celebrate your hard work by knocking out small debts and slowly working your way toward paying them all off.

For example, I have done the following:

Paying off my payday loan in the early 2000’s, I wrote the final check for $333.

Paying off my car note in 2009, once it got down to under $2,000, I wrote the final check for $1,500 and paid that sucker off!

Paying off my personal loan for $20,000, once I got down to the end, I wrote the final check for $3,500.

Paying off my credit card I got in 2005, once I got it down under $15,000, I wrote the final check (electronic) payment for $14,745, so then I could continue to live my best life.

I did this by saving up my money, paying the minimums on all my accounts until I saved up a certain dollar amount and then I wrote big fat checks to pay off what I owe. I like to pay in lump sums and pay off huge chunks of debt at a time. It makes me feel better. I call it the debt-chunk method. I like to see big results.

I got this idea from reading personal finance blogs like Millennial Money and books like I Will Teach You To Be Rich and Set For Life. In addition to studying the self-made. I combined my knowledge of reading about the money habits of Grammy-winner John Legend and Millennial Money founder Grant Sabatier.

Basically, I combined two different philosophies on saving and debt.

From John Legend I learned that once you have money in your hand you should pay off your debt IMMEDIATELY. If you have the full amount, then pay it all off. Thereby, paying off debt in huge chunks!

From Millennial Money I learned to save huge amounts of money over time by making small increases in may savings rate. I also make sure to take other good advice as well.

For instance, over the years, I have learned to listen to the following:

My partner Charlie says there is only three ways a smart person can go broke: liquor, ladies and leverage – Warren Buffett

Find ways to advertise for less or free. Leverage what you know by thinking outside the box. – Daymond John, The Power Of Broke

Find ways to start or build a business for less, cheaper alternatives out there or for $0 to start. – Zac Bissonnette, Debt Free U

There has never been a time when reading a book has not helped me. Work 10X harder, get 10X the results. – Grant Cardone, The 10X Rule

Work out. Have Discipline. Save and invest your money. I started in real estate and built wealth that allowed me to devote more time to the things I wanted to do. – Arnold Schwarzenegger

Try to save $5 a day. And increase your savings by 1% a month or more. Network. I bought coffee for those I wanted to learn from every week! – Grant Sabatier, Millennial Money

Save $25,000 to stop living paycheck-to-paycheck. Spend more on fun not less. Spend money on the things you care about and cut spending on the things you don’t. – Scott Trench. Set For Life, Bigger Pockets podcast

Spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t. – Ramit Sethi

Focus your energy on the big wins!

If you can cut your housing and car costs, your stand a chance to save $500 or more per month. That is a nice amount to start stashing away in your 401k.

Cutting out $5 lattes and couponing alone are not going to get you to amassing a fortune. But first, before you do anything, you must save!

It is far easier to control and cut your spending than it is to go out and earn more.

Besides, the more you make the more Uncle Sam takes! I am all for people earning more money, but it will make no difference if you spend every last dime.

Therefore, start focusing on slashing expenses, cutting costs, saving an emergency fund (for big expenses), a rainy day fund (for short-term expenses i.e. a flat tire) and paying off ALL YOUR DEBT!!! Doing those five things can start you on the path from broke millennial to millionaire.

And that is because all millionaires know you get there by saving $10 bucks at a time. – Mr. Money Mustache

Therefore, if you want to get rich, just start by saving $10 bucks at a time.

If you are part of the financial blog-sphere, then you have heard of a personal finance blogger by the name of Mr. Money Mustache (MMM for short).

He retired early with a net worth of $800,000.

He his famous for his no nonsense approach to cutting out buying crap and not being a Sucka Consumer. I’ll give you an example.

Physical health FIRST: whole system will only perform well if you place its wellbeing first, before anything else. Salads and barbells every day, no goddamned excuses.

Being frugal and fit, as MMM shows, has its advantages. Let’s explore this further.

1. Being frugal could turn you into a millionaire sooner than you think

While reading up on real estate, I came a cross the website Bigger Pockets and also wrote a blog post on them.

One of the co-hosts on Bigger Pockets is Brandon Turner, is an active real estate investor and entrepreneur, stated he brown bagged his lunch to work for 10 years and was able to become a millionaire by putting all his discretionary cash to work investing in real estate instead of happy hours.

2. Simple MATH is the answer

If you can add and subtract, then basically you have the skills to manage your money. Do some million-dollar math. What will it take to make the Almighty Dollar one million times? Sell 100,000 books at $10 a pop. Boom. One million.

Invest $100,000 in an index fund and let it ride for 30 years at an 8 percent return you’ve got your million bucks right there.

Basically, MMM puts it best.

And dozens of ten-dollar bills start to add up to real money pretty quickly, which is something most people don’t realize. The vast majority of wealthy people are the ones who have figured out that a millionaire is made ten bucks at a time.

-Mr. Money Mustache

3. Incomes are not as important as spending habits

Most people are pretty bad at math, even simple math unfortunately.

That partially why so many people are in debt up to their necks. If a credit card company gives you a $35,000 credit line and you are only pulling down $40,000 a year, then you can start to see right there that if you max that sucker out, you will have given away 88 percent of your income. Screw that!

On the opposite end of the income spectrum, an Amazon engineer making $175,000 a year or a Goldman Sachs investment banker making $350,000 a year that likes to tip strippers in $100’s and order $1500 bottle service could blow through a wade of cash in a few months of partying. A coke head with a nasty drug habit could snort millions and lose everything in one crazy summer.

When Google engineers are crying on the news about not being able to afford housing in San Francisco while making $200,000 a year, then something is seriously wrong out here.

They then must decide HOW FRUGAL they are willing to be to change their situation. Living in shared housing with 8 other people, living inside of a moving van, or renting a garage apartment to invest upwards of 60 percent of your income are just a few of the things you will have to consider.

It is not the size of you paycheck that matters, it is what you do with it that counts.

If you ever read that book, Your Money Or Your Life, then you know one of the authors favorite lines was yelling, “how big is yours?” He was talking about your paycheck. This guy worked on Wall St. and still managed to retire early while many folks he saw making millions were living paycheck-to-paycheck.

If you make a million, but spend one million and one dollar, sorry to break this to you, but you are still broke. It is not enough to live at your means, you must live below your means in order to have money to save and invest.

Most high-income people are still within just a few paychecks of insolvency, because it is possible to blow almost any paycheck, simply by adding or upgrading more cars, houses, and vacations.

-Mr. Money Mustache

Therefore, I urge you to slash expenses, take stock of what you have and be grateful.

Focus more on the giving than getting.

Aim at saving 20 percent or more of your income.

If you want to retire early, you are going to have to aim at saving 50-70 percent or more.

Live like it will all end tomorrow, but save like you are going to live forever. You got that? You have to save.

Who wants to be the guy living in a $500,000 home that can only afford to fill it with Christmas trees because he can’t afford furniture?

So get out there and save!!! no goddamned excuses.

Cause living in a rat infested motel is not an option because when the lights go out its a roach motel and their lease is permanent.

All I am asking is for you to do what most people won’t: Save money instead of spending it.

Let’s all welcome Michael of Financially Alert. Michael is a FIRE (financial independence retire early) blogger. He retired early after accumulating over a cool million from hard work and sacrifice while building a business. Or was it two million? Can’t remember. Doesn’t matter cause he’s here sharing part of his story with us! He graciously accepted my invitation for an interview. Well Michael you have officially been Greenback’d. 🤣

Just some quick background information.

I was introduced to Michael’s blog from a Google search I did for last years FinCon, where media meets money conference.

I was unsure if I should go or what to expect.

His website kept popping up on advice when attending a conference including FinCon. It was so thorough that I decided to do what he said and I reached out to him via email to ask if we could meet at the conference. And to my surprise he said yes!

He was pleasant, laid back, and super down to earth. He was even kind enough to send me an email and asked me to lunch! This is what it’s like meeting Michael. We ended up hanging out for a pretty good chunk of the 2nd day of the conference.

I met so many people that I couldn’t even count! So I introduced Michael to a lot of them. We could barely keep track of so many new faces.

Michael even introduced me to the founder of FinCon, PT Money.

After the conference ended, I took his advice and reached out to people to be on the blog and send invitations. And here we are today.

Let’s go!

MEET MICHAEL AND LEARN HOW TO BECOME FINANCIALLY ALERT

Starting A Financially Alert Money Blog

What prompted you to start a blog about money?

I started my blog as a way to share good money habits and knowledge with those of us who weren’t given the exposure to sound financial principles. Becoming financially alert is less about a number, and more about developing a smart and practical mindset around money. If you have the right money mindset, the mechanics are easy and your money will keep growing. I also want people to realize money is simply a tool. It can be used for good things, and likewise bad things. However, in my experience, those who feel in abundance are more likely to share with others who do not.

Why blog?

I've had people wonder what a blogger REALLY does? What is a petsonal finance blogger? Is that a real thing? Blogging about money.

Yes, sir. It is.

I and many others try to help people with financial literacy.

My blog is LEGIT!!! Put some respeck on my name!!!

“Tonight, darling, we are going to right a lot of wrongs. And we are going to wrong some rights. The first shall be last; the last shall be first; the meek shall do some earth-inheriting." – John Green, Paper Towns #papertowns

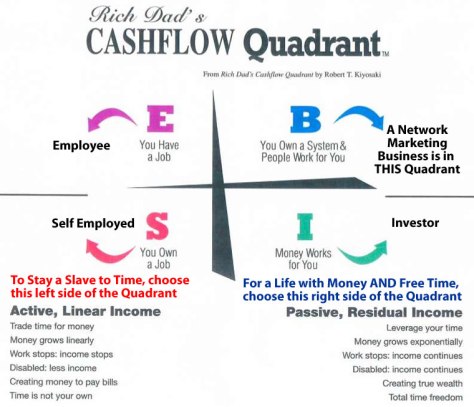

Ahh… there are so many. But, in terms of impact, Rich Dad Poor Dad really breaks things down into simple digestible concepts. I love his cash flow quadrant which speaks to the different ways people earn money.

GBM Miriam: I am providing a copy of The Rich Dada Poor Dad Quadrant for inquiring minds!

Let’s break it down.

Once you understand cash flow, you can really begin to grow your money with intention.

3. What are you reading right now? What’s on your night stand?

Dustin thoroughly guides you through the real estate investing process.

GBM Miriam: And I too love to read. I am reading several books about money right now!!!

GBM Miriam: That reminds me of the real estate website Bigger Pockets. I read their book on How to Invest in Real Estate: The Ultimate Beginner’s Guide to Getting Started. And I did a post on it.

I grew up wanting to working the movies as a special effects guy. So, when I sold my business, I took some time to myself to attend a special fx class. It was pretty fun to blow up a car – don’t try that at home kids!

In that interview, I read that you would like to travel to island with the amazing animals, it’s called Galápagos Islands. I’ve always wanted to go since I saw that video about it at the Virginia Aquarium. It looks so cool. And watching stuff blow up is right up my alley! No wonder we got along so well at FinCon18. This was a really good post. Thanks for sharing so much about yourself. I too noticed that PoF was everywhere. I had to step my game up because of him. 😉

And yes ladies and gentleman, that Tony is motivational guru and New York Times best-selling author Tony Robbins! Here is the photo Michael posted on his website. Awesome right?

See Michael’s posts on his Tony Robbins seminars a Date with Destiny and Life and Wealth Mastery

In the second post link, you will get to see Michael swinging from a trapeze in an attempt to face down his fear, which is so Tony Robbins!!!

Fun Fact: Trapeze is a piece of equipment which is used in acrobatics. It is considered to be one of the most demanding aerial arts. History. The art of trapeze performance was developed by Jules Léotard, a young French acrobat and aerialist, in Toulouse in the mid-1800s. He invented the flying trapeze, practising over his father’s swimming pool. A trapeze is a short horizontal bar hung by ropes or metal straps from a support. It can also be known as a aerial hoop, or fabric known as an aerial silk.

And Michael is still inspired by Tony Robbins all these years later. Check out one of his recent tweets 🙏😉

— Michael Quan – 𝗙𝗜𝗡𝗔𝗡𝗖𝗜𝗔𝗟𝗟𝗬 🅰🅻🅴🆁🆃 (@FinanciallyALRT) April 16, 2019

5. What’s in your wallet? How did you start building wealth?

$83 cash

4 credit cards

1 debit card

fishing license

insurance card

coupon for bare naked granola

drivers license

AA card

FINALRT Michael: I started building wealth the old fashioned way… saving! As soon as I got my first job, I started paying myself 20% automatically into my savings account. Over time it grew, and then evolved to other asset classes like stocks/bonds, and real estate.

GBM Miriam: That’s what I’m taking about!!! Take control over your finances. Control your finances, control your life. 👍

The lazy way to build a fortune: automate your savings and investments.

You can build great things when you work on things over time. Just like Voltron. 🤣I just love when things come together. Don’t you?

This is how I approached spending before I started learning about finances🤦♀️ 😂

I personally like focusing on starting salary. Negotiating a good starting salary can set you up to be even better down the line. Kind of reminds me of that scene in Clueless 🤔 starring Alicia Silverstone and Avengers Endgame Ant-man Paul Rudd.

Financial makeover. Who here wouldn’t do things differently if they knew then what they know now?

It’s like Cher (the real one not the one from the movie Clueless) said, “If I could turn back time.”

Speaking of Clueless…

I love makeovers!!!! So I wrote a post about having a financial facelift. 😉

Whatever you do, financially or otherwise…Own it!!!

I made it out of living paycheck-to-paycheck woohoo!!! I appreciate all the support from the personal finance blogger community. 💖Especially in doing interviews like this one. 😉 xoxo 💋 I feel the love. I felt just like Mulan. The finance community definitely made a man I mean blogger out of me. 🤣

Bonus Questions (pick any of the questions from the top or below that you want to answer)

6. Any life or money lessons from a favorite movie or TV show you would like to share?

TV loves to glamorize our consumer culture. While it’s fun to watch shows like Million Dollar Listing, the reality is that happiness is controlled by us individually and doesn’t required luxury items.

How can you use your money to make the biggest positive impact on your family and friends?

Well said Michael. 👏 And excellent question.

Embarrassment of riches book portrait of Scrooge McDuck and his nephews.

GBM Miriam: I have learned to not focus on having privilege, but on doing things that help myself, my family and my community. A lesson Cher (Alicia Silverstone) started to learn as the film Clueless progressed.

While shopping with her friend Dionne (Stacey Dash), she started feeling like there was more to life than shopping, like helping others. 😉

7. If you found a lottery ticket that ends up winning $2.5 million. What would you do?

After giving a chunk to charity, I’d buy a McDonald’s franchise! Who wouldn’t want a french fry cash machine??

16. What was your best MacGyver moment?

I recently was doing a video and couldn’t ad-lib the content to save my life. So, I started researching ways to help me create a better video. I stumbled upon teleprompters and was like, OMG that’s it!The problem though is that teleprompters start at $200 and go up from there. I didn’t feel like making that kind of investment for a single video, so I put on my MacGyver hat and built my own. I used an 8×10 frame from Walmart, a cheap 3 ring binder, some cork-board from Dollar Tree, and electric tape from Home Depot… total costs to build it – $12.84.

For those of you who are unfamiliar with MacGyver, here is some background info.

Angus “Mac” MacGyver is the title character and the protagonist in the TV series MacGyver. He is played by Richard Dean Anderson in the 1985 original series. Lucas Till portrays a younger version of MacGyver in the 2016 reboot. In both portrayals MacGyver is shown to possess a genius-level intellect; proficiency in multiple languages; superb engineering skills; excellent knowledge of applied physics; military training in bomb disposal techniques and a preference for non-lethal resolutions to conflicts. The hit television series MacGyver, which lasted from 1985 to 1992 and was highly successful throughout its seven-year run.

The character Angus MacGyver, also known as just MacGyver or Mac, was an optimistic action hero who was notable for using a Swiss Army knife instead of a firearm as his tool of choice.Young war hero Angus `Mac’ MacGyver has an extraordinary knack for unconventional problem solving and an extensive bank of scientific knowledge that he believes can best be put to use saving lives, both of which come in handy when he creates a clandestine organization within the United States government to tackle high-risk missions around the world. Working under the sponsorship of the Department of External Affairs, MacGyver quietly prevents disasters.

The character is portrayed as a non-violent problem solver and typically eschews the use of guns. Even in cases where he must resort to physical violence, or when his improvised devices are used to attack hostile opponents, he is always doing so in self-defense and, if possible, subduing or disabling rather than killing.

MacGyver is passionate about social causes, having on several occasions volunteered to help the less-privileged, showing a particular affinity for – and connection with – children. For example, he is shown to be a “big brother”, conducts hearing research at a school for deaf children, and helps out in a mountain excursion for delinquent youths.He strives to protect the environment and endangered species such as eagles, the black rhino,and wolves It was also established that he became a vegetarian at an unspecified date during the series run.

MacGyver’s persistence and the improvisational nature of his plans make him difficult to thwart, as his nemesis Murdoc pointed out, because not even MacGyver himself knows what he is going to do next. Unlike stereotypical “macho” or stoic action heroes, MacGyver exhibits grief in the face of tragedies, open fear in perilous situations, and shows pain after a fight. A sensitive character, Mac has a tendency to blame himself for personal losses and tragedies. He usually carries duct tape, chewing gum, a Timex watch, strike-anywhere matches, a flashlight, and an ID card. Yes, that’s what he uses to get out of every near death situation.

In short, he’s awesome.

17. How would you sell hot coco in Florida?

I’d add some ice and throw it in my vitamix for the perfect blended frozen hot coco!

Oh yea. As cool as ice!! 🤣

Thank you for stopping by Greenbacks Magnet!!!!

Hope you enjoyed this latest blogger interview. I try to keep it 💯here and help people improve the quality of their financial lives. Thank you for reading.

GBM Miriam: Thank you Michael for treating us all for an inside look to becoming financially alert. You’ve been a great guest!

Want more financial wake up calls from Michael. Follow him on Twitter and read his blog at Financially Alert.

Money is only a tool. It will take you wherever you wish, but it will not replace you as the driver. -Ayn Rand

Many of you out there I am sure have heard of Bigger

Pockets. It is the place to be for anyone interested in Real Estate (RE).

Basically, they are the Facebook of Real Estate.

Bigger Pockets (BP) is the real estate social network. You

can find out all types of things such as how to finance rental properties, find

property management companies, and how to invest in real estate.

While on my journey to learn ALL THINGS MONEY, I came across an interesting post called House Hacking.

For readers of my blog, you know I am a fan of Millennial Money (MM). Grant Sabatier is the money genius behind that site and because I was a fan of his is how I came to learn about Bigger Pockets. I learned so much from Grant that I wrote a blog post about how he inspired me to save more money.

It was on his website that I read about House Hacking, which is when you live in one of the multiple units of your investment property as your primary residence, and have renters from the other units pay your mortgage and expenses.

Like I stated on my last post, one of the biggest expenses

in any budget is housing. The trifecta of expenses is housing, food, and

transportation. If you can cut your expenses in this area, you are g2g (Good to

Go). 😉

It just so happened that he did an interview with Scott Trench

from Bigger Pockets. I am not the best when it comes to listening to podcasts,

as I prefer to read books! However, the podcast is transcribed so I read

through that. Great idea there Grant. The transcription was so good that I

listened to the podcast and just like that a fan of BP was born.

That is what made me decide to pick up the book How to

Invest in Real Estate from Bigger Pockets authored by Josh Dorkin and Brandon

Turner.

I just so happened to post a tweet and saw FINCON ask what books am I reading? So I answered and tagged the authors of the book. To my surprise, Josh Dorkin replied to my tweet and said thank you for reading and asked if I would post a review on Amazon.

Since he was polite in asking for this small request, I not only did the Amazon review (still pending as of this writing), but I also decided to review the book on my site. They say ask and you shall receive. So, I gave him a 2-for-1 and posted a review and did this blog post. One tweet did all of that.

So, without further ado…

How to Invest in Real Estate: The Ultimate Beginner’s Guide to Getting Started

THE #1 QUESTION

The reason Brandon and Josh wrote this book was to help

people. One of the most asked questions they get is, “How Do I Get Started

in Real Estate Investing?”

Well, guess what? They say ask and you shall receive, right?

Then Brandon and Josh answered.

They wrote this guide to help people along their way.

Although, the Bigger Pockets forum and blog is filled with tons of information,

it can be overwhelming. Where do you begin?

This book packs many of the interviews they do on the podcast and brings it together in one place as a reference guide.

WHAT WILL YOU LEARN

The guide contains eight chapters but my three favorites are: Chapters 1, 4, and 7.

The book will show you the following:

How to get started in Real Estate?

How to invest with no money, bad credit, and

with a full-time job?

Why you should save cash reserves?

What is an LLC? Do you even need one?

Real Estate Niches (as the riches are in niches)

😉

12 Ways to Finance your Real Estate Deals

Real Estate Exit Strategies

I think the reason people choose to invest in RE is not only

to get rich (obviously), but to have more financial control over their lives.

In addition, real estate is tangible. Unlike stocks, bonds, and CD’s you can drive by and visit with your investment. Have a cup of coffee in it. Heck, you can even live in it!

THE REAL WORLD OF INVESTING

Remember the television show “The Real World” on MTV. Well,

that was a lot of fiction and made up drama for ratings. This book provided

insight directly from RE investors with real world experience.

One of my favorite stories actually came from Chad Carson of the Coach Carson blog site. Chad decided the go big or go home route to RE was the best route for him. His niche was house flipping.

He tested this hypothesis and decided to change courses. Instead

of trying to flip 50 properties, he then decided to do less for the sake of his

sanity. This method worked.

This taught me that flipping is NOTHING like the television shows portray. We are getting the Campbell Soup version (condensed). I need the 💯 real.

You must find out what works for you. Although, you can

learn from the mistakes of others, usually trial and error will show you the

way. Fail fast, early, and hard. Then you can start to profit from your

knowledge and experience.

The book is filled with tons of stories. I just shared one.

If you want to learn more about Real Estate, then hop on over to Bigger Pockets. You can also look up some real estate blogs and books. Just like I did with this one.

Have you recently wrote a book? Are you looking for a review? Do you want to be Greenback’d? Tweet me. I’ll be here @mjp2520

![How to Invest in Real Estate: The Ultimate Beginner's Guide to Getting Started by [Turner, Brandon, Dorkin, Joshua]](https://i2.wp.com/images-na.ssl-images-amazon.com/images/I/41ZwqwL8NWL.jpg?w=474&ssl=1)

![How to Invest in Real Estate: The Ultimate Beginner's Guide to Getting Started by [Turner, Brandon, Dorkin, Joshua]](https://i0.wp.com/images-na.ssl-images-amazon.com/images/I/41ZwqwL8NWL.jpg?w=474&ssl=1)